The companies winning African tech right now don't fit your existing categories. They're not fintechs. They're not motorcycle companies. They're something we haven't had a clean word for until the numbers forced us to name it.

Call it the new stack. One part asset financier, one part payments infrastructure, one part fleet operator, one part credit bureau. Watu. M-KOPA. GoCab. Moove. These companies wear the same sector label — fintech, mobility, or both — but the business underneath is identical: use a physical product to acquire the customer, use daily repayment behavior to underwrite the next product, and let the data compound into a moat that API-only competitors cannot replicate.

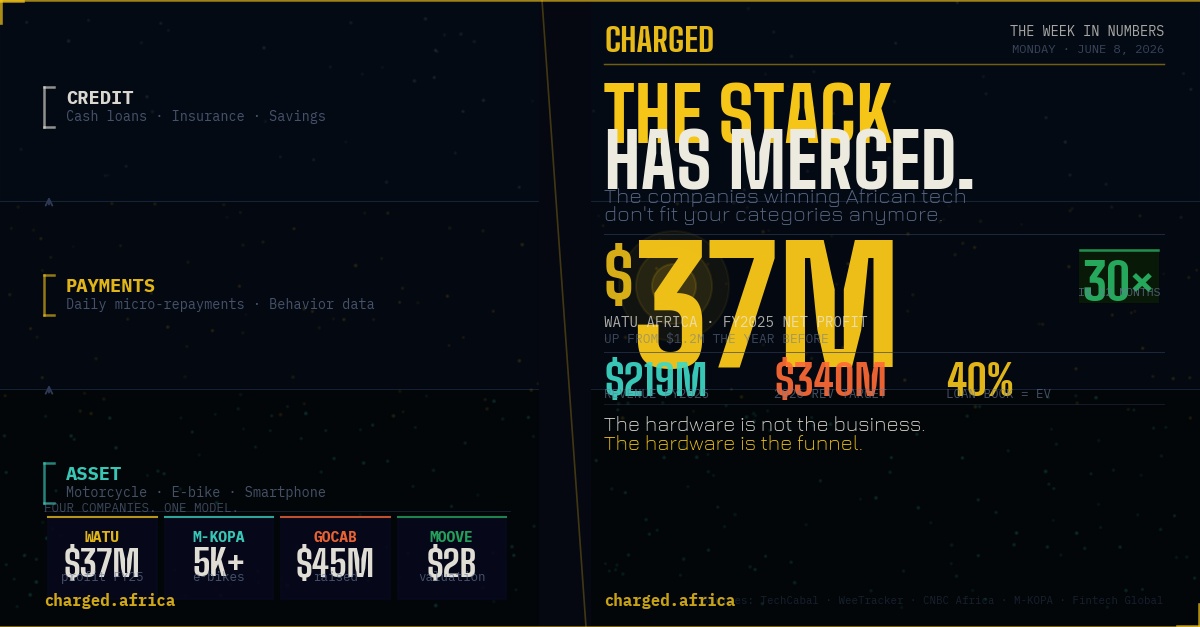

Last week gave us the numbers that prove it.

THE NUMBERS THAT DEFINE THE WEEK

$37M — Watu Africa's net profit for FY2025. That is not a typo. A year earlier, the Kenyan non-bank asset financier posted $1.2 million in net profit. In twelve months, profit grew 30x. Revenue hit $219 million — up 92.7% year-on-year. The company is now targeting $340 million in revenue by the end of 2026.

That is a hypergrowth trajectory you normally associate with SaaS businesses, not companies financing motorcycles and smartphones in East Africa. The difference is that Watu's repayment infrastructure is built on daily habit: a rider makes a swap, a payment hits, a data point accretes. At 40% of their loan book tied to EV asset financing, Watu is not hedging between mobility and credit. It has picked a thesis and bet the balance sheet on it.

5,000+ — electric motorcycles M-KOPA has financed in Kenya since launching its e-mobility product. This is the same company that used pay-as-you-go solar panels to put renewable energy in two million homes. M-KOPA understood something early that is now becoming consensus: the repayment model does not care what the asset is. A solar panel, a smartphone, an electric motorcycle — each generates daily micro-payments, each produces behavioral data, each unlocks the next product in the stack. The motorcycle is just the latest iteration of a model that has been running for a decade.

M-KOPA's broader platform has now unlocked over $600 million in credit across more than two million customers in Kenya, Uganda, Nigeria, and Ghana. The e-bike is not the product. The e-bike is the entry point.

$45M — what GoCab raised in February, two months before anyone was talking about "The New Stack." The Côte d'Ivoire-focused mobility fintech structured the round in the same way as every serious operator in this space: $15 million equity for operational runway, $30 million debt for fleet acquisition. EVs are currently 10% of GoCab's active fleet. Target by end of 2026: 50%.

GoCab is not trying to be Moove. It is planting the flag in Francophone West Africa — a market that has been chronically underfunded and where the gig-economy financing model has barely begun. Its $50 million ARR target for year-end is the milestone that turns a regional bet into a continental argument.

~$2B — Moove's last known valuation, on $250M+ raised since 2022. Uber-backed, Nigeria-founded, now operating in markets from Lagos to London, Moove is the archetype of what this model looks like at maturity. It uses Uber's proprietary driver performance data — trip completion rate, acceptance rate, cancellation rate — to underwrite vehicle financing for drivers who have no credit history a traditional bank would recognize. The collateral is the car. The underwriting is the data. The moat is the relationship that deepens with every kilometer driven.

WHAT THESE NUMBERS SHARE

Four companies, four different geographies, four different asset classes, one model.

Every company in this list acquires the customer through hardware — a motorcycle, a car, a smartphone, an e-bike. Every company builds a repayment relationship that generates behavioral data no credit bureau has. Every company uses that data to cross-sell financial products — airtime credit, health insurance, cash loans, savings accounts — that carry higher margins than the original asset financing. The hardware is not the business. The hardware is the funnel.

This is why "fintech" as a category descriptor is becoming insufficient. Watu is more accurately a data-driven asset financier. M-KOPA is a pay-as-you-go platform that happens to finance motorbikes this week and may finance something else next year. GoCab is building a gig-economy financial layer for Francophone Africa that happens to use cars as the entry product. Moove built a fintech on top of Uber's data.

None of these companies could have been built on API rails alone. The physical asset is not a strategic constraint — it is the strategic asset.

THREE THINGS TO WATCH THIS WEEK

1. Watu's expansion into Latin America. The company has flagged this move publicly. If a Kenyan asset financier builds the same pay-as-you-go motorcycle financing model in, say, Colombia or Peru, the proof-of-concept becomes a global playbook. Watch for a partnership or market-entry announcement in Q3.

2. M-KOPA's Mombasa rollout and the path to Uganda. Kenya is the test market. Mombasa is the proof that this works beyond Nairobi's boda boda density. Uganda is next and the market dynamics there (higher fuel costs, lower alternative transport competition) may make unit economics even sharper than Kenya.

3. GoCab's EV fleet mix at mid-year. The company said 10% EV now, 50% by year-end. That is an ambitious transition in six months. Watch the Q2 fleet data it will tell you whether the supply side (EV availability and battery infrastructure in Abidjan and Dakar) is keeping pace with the financing demand.

THE CHARGED READ

There is a version of this story where the convergence of fintech and e-mobility is written as a trend piece: two sectors colliding, synergies emerging, disruption incoming. That version misses what is actually happening.

What is happening is a business model clarification. The African market has been stress-testing payment infrastructure for fifteen years — M-Pesa, mobile money, agent banking, USSD rails and the lesson it learned is this: the closest thing to guaranteed repayment is a daily necessity. Airtime. Transport. Light.

Watu, M-KOPA, GoCab, and Moove did not invent this insight. They operationalized it on top of an asset the motorcycle — that is both economically essential and physically trackable. The bike has to be used to generate income. Income generates repayment. Repayment generates data. Data generates the next product.

The stack has merged because the logic was always the same. It just took the EV transition to make it visible.

CHARGED is published every Monday (The Week in Numbers) and Thursday (Deep Signal). Dar es Salaam.

Primary sources: TechCabal · WeeTracker · Launch Base Africa · Fintech Global · CNBC Africa · EV24 Africa · M-KOPA Newsroom